On Baseline's Fees

A recurring observation across the timeline: Baseline's fees are too high. It's a misread.

A recurring observation across the timeline: Baseline's fees are too high. It's a misread.

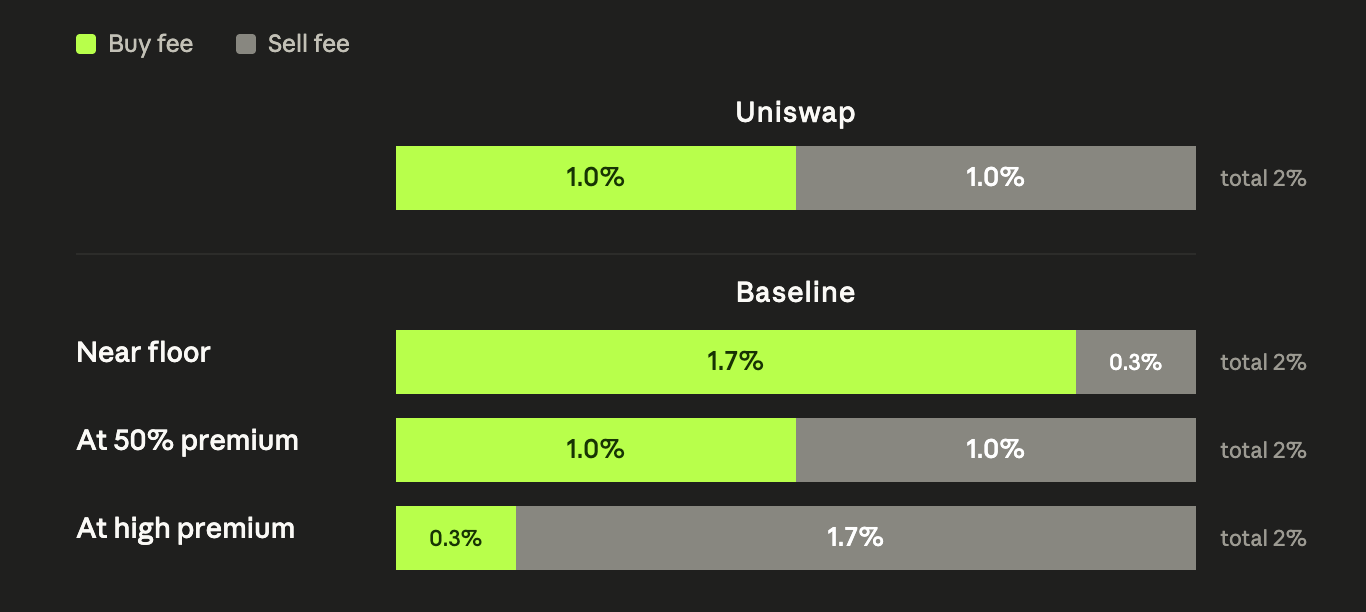

1% fee in Baseline charges the same as a 1% fee Uniswap pool. The round trip totals 2% on both. The difference is in how the fee is structured. Uniswap charges 1% on each leg statically. Baseline charges a dynamic split that always sums to 2%, weighted by where price sits relative to the floor.

Risk-Based Fee Allocation

The logic is risk-based. Every Baseline token has a guaranteed floor price (BLV) backed by reserves locked in the contract. The protocol prices the fee against the risk being taken on each side of the trade.

Close to the floor, buying is the lower-risk leg. Downside is bounded by BLV, which cannot fall. Selling is the higher-risk leg, because the seller is exiting before any potential recovery. The protocol weights the fee toward the buyer. A buy might pay 1.7% on the leg. The corresponding sell pays 0.3%. Total: 2%.

Far from the floor, the risk inverts. Buying at high premium carries elevated risk because the speculative portion of price can collapse. Selling locks in realized gain. The protocol weights the fee toward the seller. A sell might pay 1.7%. The corresponding buy pays 0.3%. Total: 2%.

The 100% premium point is where the split is exactly even. 1% on each leg, identical to Uniswap's fixed distribution. This is the only price level where Baseline's per-leg fee matches a flat-fee AMM. At every other price, the per-leg fees diverge from CPMM symmetry while the round-trip total remains constant.

The fee is embedded in price impact. There is no separate fee field on the receipt. The dynamic allocation is part of the execution price.

The asymmetry rewards behavior the protocol is designed to favor. Buys near the floor cost more on entry but cost almost nothing on exit if the trade does not work. Sells at high premium are allowed but priced. Holding through volatility is the cheapest path because the trader pays the round-trip total only when both legs complete.

Snipe the Snipers

Baseline prices every trade at the marginal price, the price at the end of the trade. Uniswap prices trades at the average price across the trade. The gap between marginal and average is borne by the trader on Baseline. For small trades, it is negligible. For trades large enough to move price meaningfully along the curve, the gap grows supralinearly.

This is intentional. It is the protocol's primary defense against bot sniping, MEV extraction, and adverse selection. A whale buying a tenth of the buffer pays a steep premium. A sniper trying to capture a launch pays the worst price, not the best. For retail-sized traders, the optimization is to split large positions into smaller sequential trades. Each trade settles at its own end price.

Holding Gets Paid

A trader who holds longer pays the same 2% on the round trip whenever they eventually sell. But during the holding period, two things happen. The floor ratchets up from other people's trades, so their downside shrinks. When they staked, they earned ETH or USD on every other trade in the pool. By the time they sell, the 2% they pay is offset, partially or fully, by the income they collected while holding.

To see what it looks like irl, head to app.baseline.markets.